Copper is set for a long bull market – here’s how to invest

Commodities are selling off a little as peace talks between Russia and Ukraine progress and the speculative mania is unwinding.

Grains have pulled back, so has oil – though daily swings of $10 a barrel now seem to be the norm – precious metals, palladium especially, are down.

War or not, most commodities will rise again – there was an ongoing shortage before Vladimir Putin went all Napoleon. But excess must be purged.

However, of note is that one industrial metal is hardly down at all, which suggests that that particular bull market has a lot further to go.

And that is why today we consider copper…

Copper is needed for everything, and supplies are low

Russia is the world’s seventh-largest producer of copper. It produces about 4% of global supply (about one million tonnes a year), and sells most of that copper to China (with some into Europe).

Iron, steel and manganese make up Ukraine’s main metallic production – it is not a big player on the copper stage.

The overall consensus was that the war and sanctions on Russia would not have as big an impact on the copper price as on other commodities – and that has so far proved the case. Bigger protagonists in the copper story lie far away – in China, Africa and the Americas.

I don’t know how many times I’ve written this sentence, or at least a variation of it, but here I find myself writing it again: China is the world’s largest consumer of copper and, despite it also being the world’s third-largest producer, is a net importer. An astonishing 54% of world copper demand is Chinese.

Europe is the next biggest user, at around 15% of demand. Followed by the Americas, the US especially, which account for another 11% of demand. Total annual demand is somewhere between 25 and 28 million tonnes (depending on whose research you follow).

Copper costs around $10,000 per tonne, so this is a $250bn-plus market. Correct me if I’ve got my maths wrong.

The country with the biggest reserves and by far and away the biggest producer is Chile. Fears of resource nationalisation there with its new-ish left-leaning government have so far proved unfounded. It produces almost six million tonnes, or 28% of annual global supply.

Next is its neighbour Peru (2,200 tonnes, 12% of global supply); China (1,700 tonnes, 8%); the Democratic Republic of Congo (1,300 tonnes, 7%); and the US (1,200 tonnes, 5%).

Copper is used just about everywhere: homebuilding, construction, manufacturing, power generation, electronics and transportation. Which is why demand is often seen as a barometer of economic health. Overall demand is split roughly 65% electrical, 25% industrial and 10% transportation.

China’s inventories are at their lowest levels in four years (since before the pandemic), as are London Metal Exchange (LME) inventories, as is global visible inventory generally, suggesting strong support for current prices.

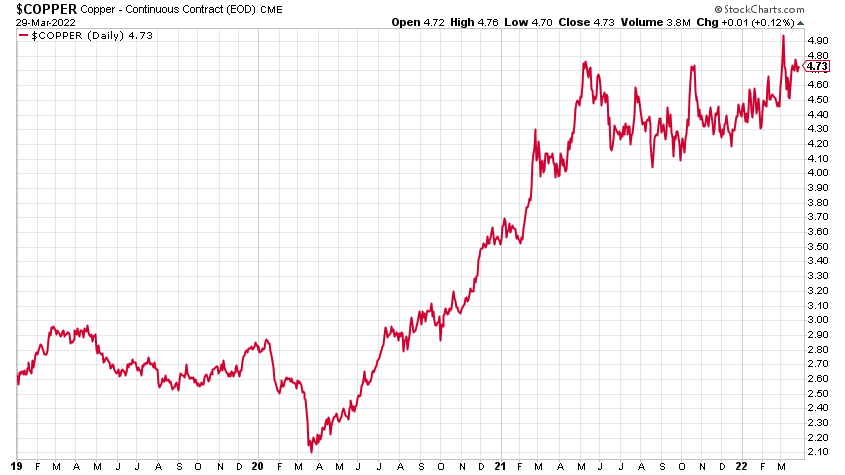

What does the copper chart tell us?

So to the copper price. It had a huge run up in the bull market of the 2000s. It collapsed in 2008, rallied again to a peak in 2011 (around $4.60/lb), and then went through nine years of bear market, during which it lost more than 50%.

It successfully retested its lows around $2/lb in 2016 and 2020. It then went ballistic in the post corona-rebound, reaching new highs in 2021, since when it has been consolidating around the new highs.

Here is 20 years of copper:

And zooming in, here is three years of copper, so you can see the consolidation of the last year, steadily creeping higher.

The Dominic Frisby house call remains: “own copper”. It wants to go higher.

Never mind China, if we are to have our Green Revolution, we are going to require a lot more of it.

So how to invest?

There is no shortage of methods, depending on your risk appetite – from futures to exchange-traded funds (ETFs) to spread bets to stocks and shares.

You can even go down the scrapyard and buy the metal itself. That is what one of my brothers-in-law used to do. But he is mental.

If you want to simply play the copper price, without taking in individual company or mining risk, there is the Copper ETF (LSE: COPA).

Then there are the miners. If you don’t want individual company risk, there is even an option for you there: the Global X copper miners ETF, the most liquid version of which is listed in New York (NYSE:COPX) but there are also “subsidiaries” in London, denominated in dollars (LSE:COPX) and sterling (LSE:COPG). The latter is probably the best way to avoid broker forex charges, though you’ll end up paying them by the back door.

London has no shortage of options when it comes to mining companies. There are the giants: BHP Group (LSE:BLT), plus Glencore (LSE:GLEN), Anglo American (LSE:AAL), Rio Tinto (LSE:RIO), and Antofagasta (LSE:ANTO).

US-listed Freeport-McMoran (NYSE:FCX), the world's second-largest producer (after Chilean state-owned Codelco), should also probably get a plug, as it’s a purer play than most of the mining giants, Antofagasta aside.

There are plenty of smallcaps and midcaps to spice up your dinner, or give you indigestion, depending on how much you consume. I’ll put together a Special Report in due course. Canada and Australia probably have the most listed, although there are also plenty on London’s Aim.

Just remember what Mark Twain said: “a mine is a hole in the ground with a liar standing next to it”. Or words to that effect.

Check out my Special Report on tin, if you haven’t yet already seen it.

This article first appeared at Moneyweek.

LSE-AIM, I'd agree with the analogy about mines & liars.

I've only recently started sniffing around these parts again, I turned my back on LSE and AIM listed small caps in about 2008 / 2009.

With exception of a handful of dual listed large caps, (e.g. BHP), I gave up, in favour of North American large caps.

As you highlighted in the tin report, so many of these companies on AIM are run by shysters, with nothing but contempt for the shareholders.

Often, the retail shareholders are elbowed out, by a variety of methods, e.g. high interest loans & bond issues which can't be met, share options, penny in the pound takeouts, transfers & sales of assets to affiliate cos etc etc - the end result that the original shareholders get fleeced and end up owning nothing.

Sure, some of these cos probably start with the best intentions & simply end in financial difficulties - but others, I doubt had any intention of taking the original shareholders anywhere other than the cleaners. Sad thing is, the same names keep cropping up, often in multiple companies at the same time.

What is Stephen Dattels up to these days?

Even some of the quality projects like Sirius Woodsmith mine (despite being in the most expensive jurisdiction on the planet), looked promising - where are the original shareholders? who owns it now?

Apologies for the rant - be careful out there. Keep up the good work!

(With regard to copper, I currently hold, FCX, BHP, VALE, AAL, RIO)

VALE is primarily iron ore & pellets, but the nickel segment in particular, given where we are, is NOT insignificant, they have a record for distributing free cash to shareholders.