Bull markets don’t last forever. When you’re in the throes of one, it can feel like they do. But they don’t, and at a certain point you have to sell.

Gold bull markets can feel even more eternal. Not just because the metal itself is eternal, but because the story comes along that we are going back to a gold standard, or that the Great Purge, which many economists of the Austrian school say is inevitable after fifty years of fiat decadence, is finally upon us.

I get that argument. But it is too neat, too deterministic. Real life is much more mucky.

So today I want to consider a very important question, and I want to try and answer it honestly:

Where are we in this bull market?

Has gold already peaked? It’s possible. The spike to $5,600/oz at the end of January had many of the hallmarks of a blow-off top.

Or perhaps $5,600 was just a mid-cycle peak, such as we saw in 2006 or 1975-76 during previous bull markets.

Or is this bull market still in its infancy?

I’m going to study this bull market through every lens I can think of: price, time, valuation, participation, market structure, macro context and sentiment.

My bias going in is that we are mid-cycle, as I argued in my Great Forecast last week. Let’s see where I end up.

1. Duration

There have been two great gold bull markets since the end of the gold standard: 1971-1980 and 2001-2011. Both lasted nine to ten years.

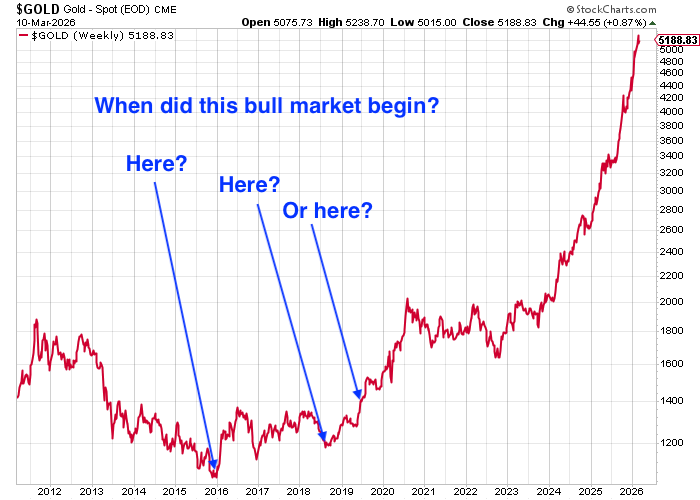

When did this one begin?

It depends how you define it.

You could take the bear-market low of $1,045 in late 2015. You could take the $1,160 retest in 2018. You could take 2019, when gold broke out of its multi-year base.

Technical analysis is often in the eye of the beholder. Just like bull markets.

You could even argue late 2022, when the current acceleration began.

If you start in 2015, this bull market has already lasted ten years. That would put it right in line with the duration of previous cycles, and you could argue it is close to exhaustion.

If you start in 2018 or 2019, there may be several years left to run.

I favour 2018. Just as gold hit $250 in 1999, rallied, and then returned to roughly the same level in 2001 before the real bull market began, the 2018 low feels like the equivalent retest. Of course this is debatable.

And there is always the possibility that this bull market lasts longer than previous ones.

Verdict: mid- to late-cycle.

2. Relative valuation vs other assets

Oil

With gold at $5,200 and WTI crude around $87, it takes roughly 60 barrels of oil to buy one ounce of gold.

Historically this ratio ranges between 6 and 30.

The only time oil has been this cheap relative to gold was in the 2020 pandemic collapse, when oil went negative.

My view: it’s not so much that gold is expensive as that oil is cheap. Plus commodities inevitably get cheaper as we get better at producing them. (As long as you don’t measure the price in fiat).

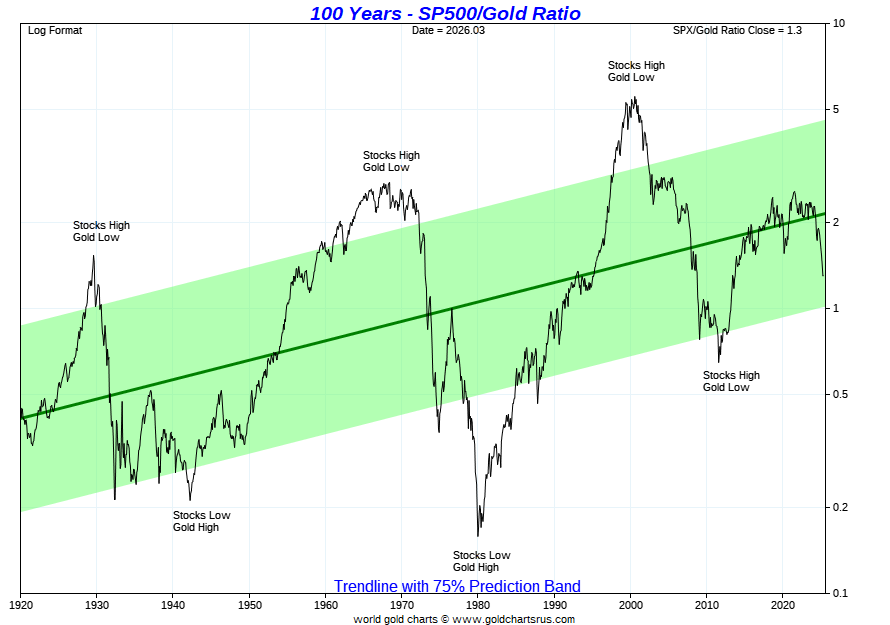

Gold vs the S&P 500

With the S&P around 6,765, it takes about 1.3 ounces of gold to buy one unit of the index.

This ratio has been as high as 5 - at the peak of Dotcom in 2000, and the nadir of gold - and as low as 0.2 (during the depths of the 1930s and at the 1980 gold peak).

Gold is therefore on the expensive side relative to equities, but not at historic extremes.

This ratio could fall further if equities fall or gold rises.

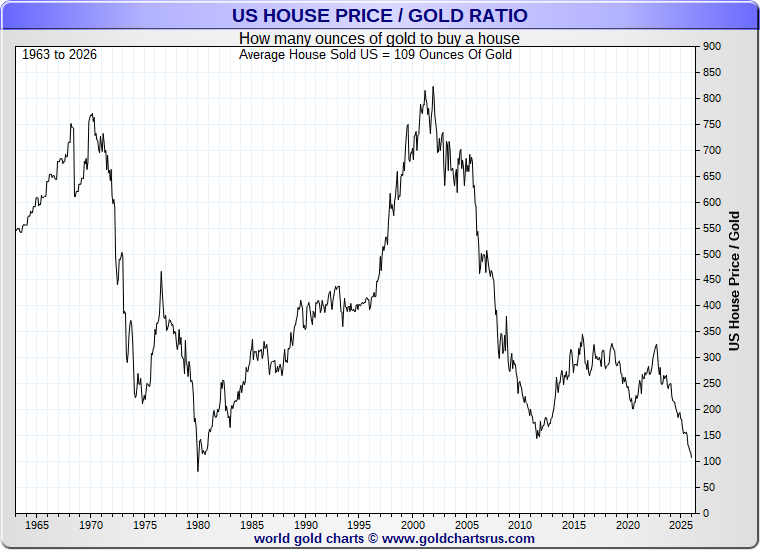

Gold vs US housing

The US housing market varies enormously by region - Beverely Hills is not Detroit, Miami Beach is not McDowell County - so national averages should be treated cautiously. But they still give a rough guide.

We are now below the 2011 level and approaching 1980 territory in terms of how many ounces of gold buy a typical home.

Pretty extreme.

Overall verdict: late-cycle. Warning signal

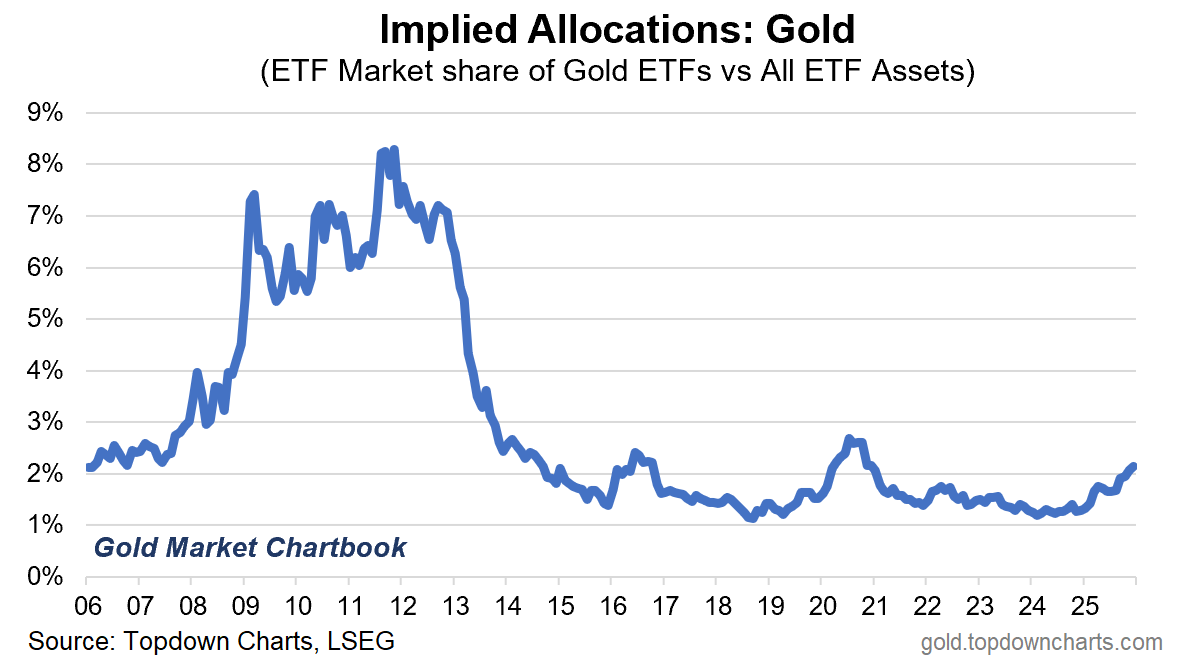

3. Institutional ownership

Gold is still under-owned in institutional portfolios.

Even after the recent rally, gold represents only a tiny fraction of global portfolio allocation compared with equities and bonds.

Gold mining equities are even more neglected.

Verdict: mid-cycle

4. Central banks

Central bank buying slowed to 863 tonnes in 2025, down from record levels in 2024, but still well above the 2010-2021 average.

However, the World Gold Council reported that central banks purchased only 5 tonnes in January, below the monthly average of 27 tonnes. I would not read too much into that. Much buying is reported with delays, and China in particular reveals little about its activity.

The usual assumption is that central bank buying is an early or mid-cycle phenomenon. I am not entirely convinced. If the real driver of this bull market is de-dollarisation and reserve diversification amidst a wider geopolitical shift, then official buying could persist for years.

Gold currently represents just under 30% of central bank reserves. The US dollar still accounts for roughly 56%.

I don’t think this bull market ends until gold sits north of 50% having overtaken the dollar itself.

Question: is the war in Iran going to arrest of accelerate de-dollarisation? You know the answer.

Verdict: mid-cycle

5. Retail participation

Retail demand is growing. 2025 saw record bar and coin demand. ETF inflows are rising, but they are not exploding. Mining companies are finally attracting interest again.

Silver went briefly manic last month, which is not a healthy sign, but the episode is already unwinding.

Verdict: mid-cycle

By the way, due to its senior currency status, the US dollar is going to preserve its purchasing power better than the pound, which is a car crash waiting to happen. I keep getting asked, “is it too late to buy gold?”. If you are in the UK, . We are turning into South Africa and the currency will go the same way. The 40% loss of purchasing power that the pound has seen since 2020 is not going to reverse. If anything it accelerates. Thus …

If you live in a third world country such as the UK, I urge you to own gold or silver. The pound will be further devalued, as will the euro and dollar. The bullion dealer I recommend is The Pure Gold Company. They deliver to the UK, the US, Canada and Europe. More here.

6. Leverage

Leverage is difficult to measure precisely.

You can look at: futures positioning on Comex, options activity, speculative flows into junior miners, retail spread betting and more. The short answer is this: gold is a crowded trade, but it is not a mania.

If it were a mania, the geopolitical shock in Iran last week would have triggered violent liquidations. Instead gold held up remarkably well.

Verdict: mid-cycle

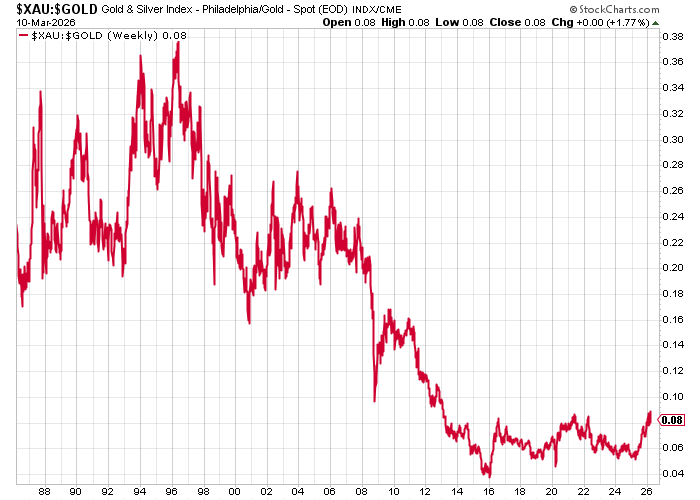

7. Mining equities

Mining stocks had an excellent 2025. Word is that PDAC last week (the world’s largest mining conference), was the like of which had not been felt since 2011 and the last top. That is a warning sign.

This chart shows the ratio of the XAU (large mining companies) to gold since 1988.

On a relative basis the miners are still phenomenally under-owned, and we now have a text-book base, formed over 9-years, in place. If this ratio goes back to levels of the early 0 0s , miners will multiply many times over.

But these declines began with the emergence of the ETFs and the many alternative ways to own gold without taking on individual company risk. The ratio does not have to go back 00s levels.

Maybe. But that base is a thing of beauty.

Typically the end of a gold bull market would coincide with massive rallies in junior miners, an exploration IPO boom and a merger-and-acquisition frenzy.

We are seeing healthy signs of activity, but nothing like that yet.

Verdict: mid-cycle

I’m delighted to report that The Secret History of Gold - Myth, Money, Politics and Power, published by Penguin Life, comes out in the US next month. (The US version is published by Pegasus). Order yours now - via Barnes and Noble or Amazon

8. The narrative - gold to $150,000?

Gold got some coverage in publications like The Economist and the Financial Times last month, but the story is far from mainstream.

Ask most people about de-dollarisation, Triffin’s dilemma or central bank reserve diversification and you will get blank looks.

However, some familiar late-cycle narratives are beginning to appear.

One is that silver is being remonetised.

It isn’t.

Silver may well be an important strategic metal, but its monetary role was as medium of exchange. That role is not coming back because we no longer use physical money. That function has been digitised.

Gold, by contrast, retains its role as as store of value - a function that silver never had to anything like the same extent. Silver may have use as a speculative asset. It may well rise in price. It may even overshoot spectacularly. But it is not being remonetised. That will not happen, unless Eastenders turns into Mad Max.

Another narrative that sometimes appears near major peaks is the US national debt relative to gold reserves. In 1980, headlines declared the US was “solvent again” because it could have used its gold to fully settled its debt.

Today US debt is roughly $39 trillion. To settle that debt using America’s 262 million ounces of gold, the gold price would need to be roughly $150,000 per ounce.

When arguments like that start circulating, it means the narrative can’t go much further and the cycle is close to exhaustion.

We are not there yet.

Verdict: mid-cycle

9. Real yields

Last but not least: real interest rates.

This would be the 10-year Treasury yield minus inflation, or the 10-year TIPS yield.

Gold bull markets tend to end when real yields rise sharply.

In 1980, Paul Volcker pushed interest rates toward 20% and real yields surged. Gold then entered a twenty-year bear market. At the 2011 peak, real yields rose from deeply negative to positive and gold topped within months. From 2020–2022 real yields went negative again and gold surged, until they rose in 2022 and gold stalled.

Today nominal yields are relatively high, but inflation remains elevated, the Fed is under pressure to ease (as are most central banks) and fiscal deficits are enormous.

Real yields therefore sit around zero or slightly positive, depending on how they are measured. That is not restrictive enough to kill the gold bull market.

The danger signal would be inflation falling sharply while nominal yields stay high, pushing real yields well above +2%. We are some distance from that.

Verdict: mid-cycle

If you are interested in following the real yield argument, Charlie Morris is the man. He gets it better than anyone, and I heartily recommend you follow his work via his Atlas Pulse. Get your copy here - it’s free.

Conclusion

If gold continues rising it will pull silver and mining equities higher with it.

The spike in silver last month to around $125 looked very much like a mid-cycle blow-off, and a period of consolidation is now both likely and healthy.

Looking across all the indicators, most point toward a mid-cycle environment rather than a late-cycle one.

Duration and relative valuation raise some concerns, but these are just one or two of nine indicators. Everything else suggests the bull market has not yet reached its final, most speculative phase.

In other words: this is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning.

$8 to $10,000 by the end of the decade is a very real possibility.

Thanks very much for being a subscriber to Flying Frisby.

Until next time,

Dominic

PS I have discussed gold largely in dollar terms, because the market is quoted in dollars. But if you are in the UK the case for owning gold has less to do with the dollar and far more to do with the pound. Sterling has already lost roughly 40% of its purchasing power since 2020, and that trend is not going to reverse. If anything it will accelerate. It’s not just the ineptitude of successive governments, but unelected permablob (in this case the Treasury, the OBR, the Bank of England, the FCA et al) that actually runs the show. The system- if you can call it that - is the problem and it’s not going to change. The incentives are to spend more, borrow more and debase the currency slowly over time. You cannot fix that system. But you can protect yourself from it. And that means owning some gold.

Disclaimer

I am not regulated by the Financial Conduct Authority (FCA) or any other regulatory body as a financial advisor. Therefore, any information provided in this newsletter does not constitute regulated financial advice. It is solely an expression of opinion. Small-cap stocks are inherently risky. Please conduct your own due diligence and consult with a financial advisor, if you have any doubts. Remember, markets can both rise and fall, especially in the case of small and mid-cap stocks. I am not aware of your individual financial circumstances, so only invest money that you can afford to lose.