How to Invest in Platinum

A special report and an update

Before we begin today’s piece, I just wanted to draw your attention to Mining Journal Select London on March 27-28, which may be of interest. The event is free to investors, and will bring a selection of mining companies with rated projects to present to an audience of over 400. Plus there are panel discussions (I will be speaking on one), spotlights and a meeting planner which gives investors a chance to meet the execs from leading mining companies. Register here.

So to platinum …

These past five years have seen most metals have a brief moment in the sun, but not so much platinum, which has been wretched. Platinum is up there close to silver for its propensity to disappoint. Its day will come. The question is when.

But I note with some optimism the relative strength it has displayed in the volatility of the last few weeks. Moreover, last week the World Platinum Investment Council (WPIC) published its Platinum Quarterly (for the fourth quarter of 2022), revising its forecast for 2023, and it is quite promising.

After two years of surpluses, the platinum market is forecast to move to a material deficit in 2023. The swing is considerable. There was a 776koz surplus in 2022. That will become a 556koz deficit in 2023. That translates to a 24% increase in demand but just a 3% increase in supply. (Supply was down 12% in 2022).Where is the demand going to come from?

The three main sources of platinum demand around the world are industrial, especially automobiles, investment and jewellery. The auto market is set to see 10% increase in demand, says the WPIC; other industrial demand 12% increase; both jewellery and investment demand are also forecast to rise.

Platinum is used in the automobile industry in catalytic converters to oxidise the carbon monoxide in diesel engines - that’s why catalytic converters keep getting nicked - for the platinum (palladium is used in petrol engines, and the thieves want that too). Global automotive demand is on the increase. We are not yet at pre-pandemic levels, but demand appears to be shrugging off issues arising from lockdowns in China, the war in Ukraine, chip shortages and cost-of-living concerns.

For platinum specifically, 2022 saw a 28% increase in hybrid vehicle manufacture, tighter emissions legislation in China (which means more platinum for heavy-duty diesel vehicles) and greater substitution of platinum for more expensive palladium (that won’t last as the palladium price has come down by 50% from its highs (ouch).

Industrial demand is largely coming from Japan and China, and from the glass industry. Jewellery demand from China is also forecast to increase as lockdowns ease.

The big eventual kahuna for platinum is the so-called hydrogen economy - green hydrogen and fuel cell electric vehicles (FCEVs). Platinum is used in water electrolysers to produce green hydrogen, and also in hydrogen fuel cells, which can power fuel cell electric vehicles. It is key to unlocking hydrogen and will thus be key to meeting global net zero targets. At present, European policy-makers have bet the farm on electric motors. Japan, however, seems to be going down the hydrogen route to decarbonisation. Given that the ultimate source of most electricity is the burning of fossil fuel, it seems, to this author at least, that hydrogen will prove the better option. This is all well known, however, and currently the market does not seem to care.

“While hydrogen-related demand for platinum is relatively small in 2022 and 2023, hydrogen-related demand for platinum is expected to grow substantially through the rest of the decade and beyond, reaching as much as 35% of total yearly platinum demand by 2040,” says World Platinum Investment Council (WPIC) research director Edward Sterck.

Sterk thinks FCEV demand for platinum will eventually equal current automotive demand, perhaps as soon as 2033 if there is broad commercial adoption, meaning there will be an added three million ounces of annual platinum demand.

Platinum supply

On the supply side, the issues are South Africa and Russia. The former has the perennial spectre of “operational challenges” and power supply risks looming over it, while the latter has been frozen out of much (but not all) of the global economy.

The big fish in the platinum pond is one small region South Africa – the Bushveld, three hours drive to the northwest of Johannesburg. Roughly 75% of annual global supply comes from there.

With this central point of failure, the market is vulnerable. Should something significant go wrong – strikes, political disruption, power supply failures, some kind of natural disaster – the platinum market has big problems. Platinum longs will do very well.

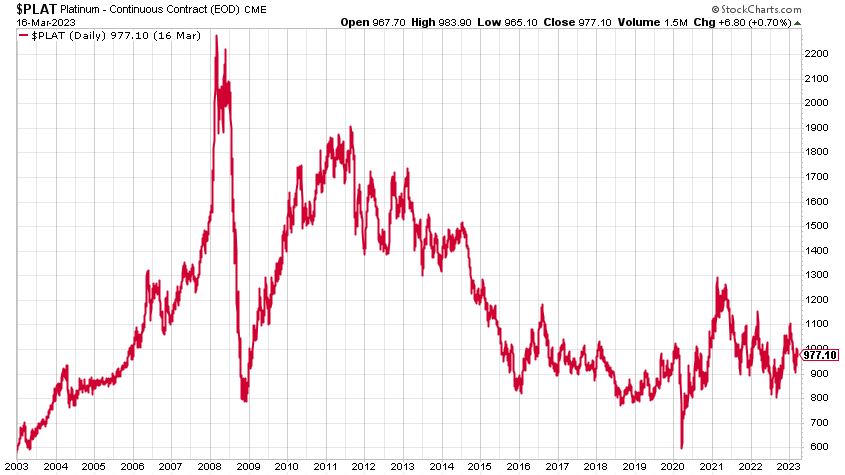

Strikes and power failures were both catalysts in the 2000s, when platinum enjoyed an epic run north of $2,200/oz.

Today it sits at around $970. In these inflationary times, it is hard to find an asset so far off its highs. But when it comes to disappointment, platinum, like silver, can be relied on to deliver.

In our psyche, platinum is more expensive than gold. That’s why platinum credit cards are of higher status than gold and why, in the world of album certification, platinum (one million units sold) ranks higher than gold (half a million units).

Platinum is also rarer than gold, which is why it “should” be more expensive. In 2008 it was more than double the gold price. The historical average is 1.25 times. With gold sitting at around $1,950/oz, you would expect the platinum price to be trading above $2,400. No such luck. It’s half the gold price.

The chief villain in platinum’s failure of recent years was the Volkswagen diesel scandal of late 2015 – when it emerged that diesel engines weren’t quite as clean as they were made out to be. The platinum price was already falling by 2015, when the scandal broke, along with other metals, but as demand for diesel vehicles fell, especially in Europe, exacerbated by unfavourable taxation and regulation, platinum could never really recover.

There is also the fact that, though precious, platinum is not a monetary metal, so the speculative, anti-inflation trade that buys gold, silver or crypto does not so much buy platinum.

Meanwhile, as far as jewellery is concerned, platinum is not as fashionable as it was 10 years ago – perhaps because it is worth less, ironically, and jewellery is a status symbol.

But jewellery demand appears now to be picking up, and the fall in demand for diesel has now levelled off. Those figures from the World Platinum Council suggest that, after many years of flatlining, the platinum story may be getting ready to roll once again. That said: the lesson of the last 15 years is to never underestimate platinum’s propensity to disappoint.

Three stories could drive the platinum price

There are three potential stories that could precipitate a dramatic change in platinum’s fate.

A change in attitude towards diesel.

The hydrogen economy takes off.

Something goes wrong in South Africa. (Perhaps the most likely).

Over the past year, platinum has ranged between $800 and $1,200. At the moment it is in the middle of that range, having displayed some impressive relative strength in the market volatility of the past few weeks.

Platinum’s doldrums may continue for the time being. But one day it will all look very obvious that everyone should have some platinum in their portfolio.

If you can pick up platinum close to $900, I can’t see how this goes wrong as a long-term investment – but, as I say, you may have to wait a while for the investment to come good.

A return to ‘normal’ historical ratios between platinum and other metals could see it easily double.

Ways to invest in platinum

As with gold and silver, there are two main ways to play the platinum story. You can either buy the metal itself, or some derivative thereof, or you can invest in a company that mines the metal.