Summer of Gold, Part 1: A Second Chance

The original investment case failed. Has management built a stronger one?

Greetings from Vegas

Never have I experienced a place so focused on separating you from your money. It’s worse than junior mining.

It’s relentless. Just getting from reception to your room without losing your shirt is a win.

I’m enjoying my experience here but I’m not sure Vegas is for me. I like fresh air. I didn’t see daylight yesterday and I only realised after it had got dark

Before I forget: I promised Liz Truss I would plug CPAC UK which runs from July 16-18 in London. Speakers include the former PM, Nigel Farage, Jacob Rees Mogg and Yours Truly . No Count Binface as far as I’m aware.

Flying Frisby readers can get 25% off with this link.

So to the matter at hand …

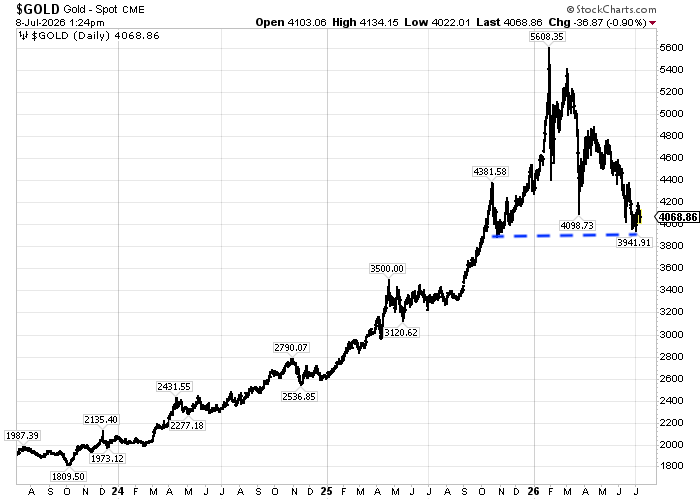

Iran bombing certainly took all the speculative money out of the precious metals trade. Both gold and silver have been grinding lower ever since, so that we are now well and truly in a downtrend.

I suspect we are nearer the lows now than we are the highs. The bullion dealers are all saying it. There are so many signs of capitulation, plus it’s the summer, always the weakest time of year for gold. But I also expect to have another 6 months of churn

Looking at the 3-year chart, the downtrend is clear. I see support of $3,900, for reasons explained by the blue dashed line.

Failing that we go back to the $3,300-500 zone, where there is a lot of support.

I still feel silver wants to touch back at $50, if only to kiss it goodbye.

On the other hand, gold is $4,000 an ounce. A year ago $4,000 seemed almost fanciful. Mining companies should be making a great deal of money. Albeit with brief interludes, mining shares have underperformed the metal for years, often deservedly so. Too much dilution, too long to get to profit (not always their fault), too much hype, not enough substance and too many alternative ways to play the gold story without taking on individual company risk.

The right miner, however, can multiply your money.

I buy a lot of speculative explorers because I sometimes get offered placements, warrants and the like, but cannot always write such things up because they are not suitable for everyone. Moreover they are not always core holdings. There are plenty of companies with established production, close to production or with assets that for some reason are undervalued. Over the course of the summer, I am going to devote a lot of commentary of these.

My position remains that gold trades sideways for a year as it churns through the excesses which peaked in January. I see this as a mid-cycle correction rather than the end of the bull market. Think 2006 rather than 2011. I’m still looking for $7,000 to $10,000 gold before the decade is out

In such a situation, you want to own some mining companies, and at the moment they are trading as though gold were trading below $3,000. In deed many of the valuation metrics are built around ~$2,000.

I do not see this publication as a tip sheet and these are not intended as a list of tips. Rather, I want to explain how I think about them today. Has the original investment case strengthened or weakened? What has management delivered? What are the next catalysts? At what point would I consider selling?

And we are going to start with what is my second largest position, a company that has changed considerably since I first wrote about it on here many moons ago. Even its name has changed and it deserves a fresh look.