Today we return to one of my favourite subjects, and one that we periodically visit: UK house prices measured in gold.

As regular readers will know, I am firmly of the mind that unaffordable housing in the UK (and indeed across most of the developed world) is as much a consequence of our system of money and credit as it is of dumb, prohibitive planning laws.

If interest rates reflected actual inflation, the story would be very different. I’m not talking about the consumer price index (CPI) measure targeted by the Bank of England (and even that now stands at over 6%). I’m talking about the inflation of the money supply, whether via debt expansion or quantitative easing (QE), and the resulting costs felt.

House prices are currently rising at roughly 11% a year, and you’re telling me inflation is only 6%? Pull the other one.

The incremental effects of these rises – 7% one year, 12% the next – over many decades have made house prices ludicrously unaffordable to young people. It’s been going on since at least the early 1990s, and the days when Ken Clarke was chancellor, and before. Salaries have not kept up.

If interest rates rose to reflect our current 11% house price inflation then the ensuing rush for the exit would pretty quickly make house prices affordable again. The entire house-of-cards economy would come crashing down too, but that’s another matter.

For this reason, we conduct the occasional exercise of measuring house prices in sound money. Gold has served this role since the Stone Age, and so we bow to the wisdom of Mother Nature, and use it here.

The pound in your pocket has lost a lot of value compared to a house…

The average price of a house in the UK is now £274,000 according to the Office for National Statistics and the Land Registry. The average salary is £31,285, so house prices are at roughly nine times earnings.

The house-prices-to-earnings ratio in most big cities, especially in the south, is much more distorted than that. It was three times when I bought my first flat in London in 1993.

We’ll start with house prices in pounds.

This chart goes all the way back to 1953, when mortgages barely existed. Debt is the big driver of house prices – if there is no debt in a market, prices will reflect local cash levels and be much lower. Introduce debt, and up go prices. (Debt, even with all that QE, remains the biggest supply of new money).

On the other hand, debt makes it possible to do things now you would otherwise not be able to do – like buy a house.

But keep debt costs low and more money enters the system, prices stay high and the economy “grows”. That’s why the authorities prefer to keep interest rates down.

“You’ve never had it so good”, was the government’s cry at the time, as the Tories actively encouraged a “property-owning democracy”. Stamp duty was cut and the government lent money to building societies, so they could issue mortgages. Home ownership rose from 29% in 1951 to 45% by 1964, and the train of higher prices was put in motion. They rose by over 50% during that period.

The above chart is astonishing in its relentless rise higher. It looks like bitcoin! The crash of the early 1990s, in which hundreds of thousands of people lost their homes amid surging interest rates, is a mere blip. Far fewer lost their homes in 2008, because rates were slashed.

But looked at from another perspective, you can see just how much value your money has lost. In 1953, the average house cost £1,891. Today it’s 150 times that. The pound has lost more than 99% of its purchasing power in 70 years.

Money. Huh! It’s a fraud. But you can’t do without it.

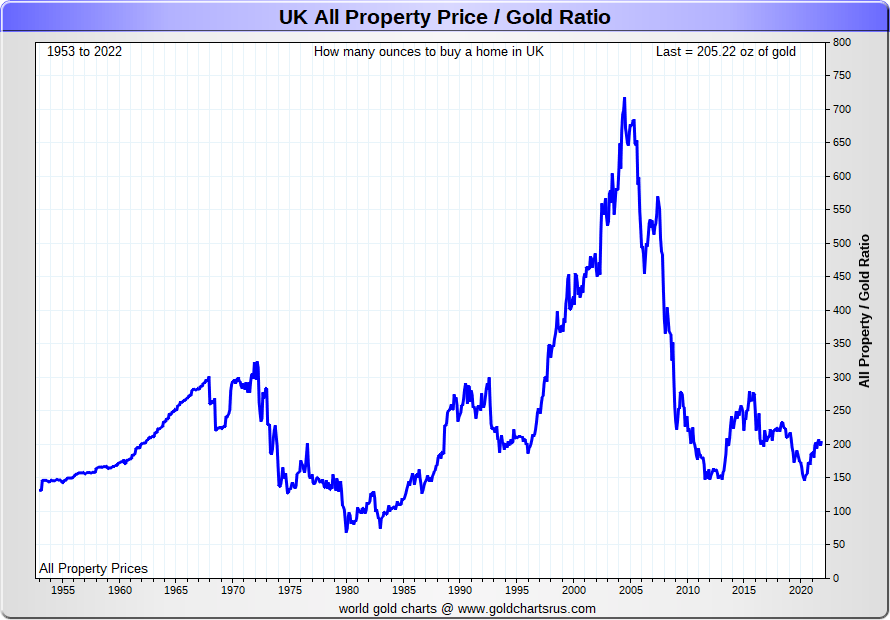

… but the gold in your vault has not

Next we turn our attention to UK house prices measured in a much sounder form of money - one that central banks can’t print. This is the same house prices measured in gold since 1953.

As you can see, it’s rather a different story.

Back in 1953 the average house cost 150 ounces of gold. Same price as in 2020.

Wait a minute, what?

And today a house will cost you 205 ounces of gold.

Wait a minute you’re telling me house prices are only up 30% since 1953?

If you measure them in gold, yup.

In 1980 you could buy the average UK house for 50 ounces of gold. You could have done so in the 1930s as well (not shown on the chart).

In 2004, with gold sitting at around $400 an ounce, and the average house at £150,000, it took over 700 ounces to buy a house. The noughties aside, the long-term “normal” price of a British house in gold terms ranges between 150 and 300 ounces.

So what’s next for the house price to gold ratio?

I thought the end was nigh for the housing bubble in 2007. I was wrong. I didn’t foresee interest rates being slashed like that. Woe betide anyone who calls the top in housing. The only thing that will send house prices lower is increased rates – though even at 3% or 4% there would be problems.

No policy-maker wants falling house prices on their watch, partly because they own houses, partly because of the damage to their reputation and partly because they don’t want to see people lose their homes (never mind those who can’t afford). So I very much doubt that we will see rates reach the levels that real (and even CPI) inflation suggests they should be.

Perhaps the Bank of England’s hands will be forced, maybe by problems in the gilt market, spiralling food and energy prices, or the rising cost of de-globalisation. Even so, never underestimate the ability of central bankers to print and obfuscate.

On the other hand, gold looks like it wants to go higher. It’s gold – it has a propensity to disappoint (to put it mildly), but, from war to riots to inflation, it is not like there is currently a shortage of fundamental drivers to push it higher.

So I would argue that that ratio will come back to 150 ounces a house before it goes to 300.

And, who knows, a little bit of a crisis will send it back to 50 ounces.

“Yes, yes”, my father used to say. “But you can’t live in gold. And gold doesn't pay rent.”

He has a point. But so do I. Central banking has left a generation homeless. Fiat money has done terrible things to society.

Thanks very much for reading/listening. Sign up to my Substack if you haven’t already. Lots more quality content coming. Share this article with a friend if you liked it and check out my paid letter - our stocks are doing pretty well at the minute.

This article first appeared at Moneyweek.

Here it is in video form: