Good morning to you,

Sunday’s piece on the inexorable rise of the far right and what to do about it has struck quite a few nerves. Check it out here, if you haven’t already.

In today’s piece - considerably less political - which was first published in Moneyweek last Friday, we consider the sorry state of junior mining.

Enjoy!

Dominic

Mining is infamously cyclical. But if ever there was an industry that blows desert hot and arctic cold, it is the subsector of small cap and early-stage companies known as junior miners. And boy has it been blowing cold.

Many of the old hands are saying this is the worst bear market they have ever known. Worse than the 2013-15, when junior mining had a near-death experience, following the boom of the 2000s; worse than the bear market of the 1990s that came with colossally depressed metals prices at the end of a 20-year bear market and then the Bre-X scandal.

Bre-X was one of the scams of the century. The Canadian gold mining company falsified gold samples from its mine in the middle of nowhere in Indonesia. The stock went up over 1,000-fold, from pennies to a C$6 billion valuation, before the fraud was exposed. Many were defrauded and the sector went into a prolonged depression, starving it of capital. The story became the basis for the film, Gold, starring Matthew McConaughey.

Mining needs capital. It typically takes more than 15 years to take a mine from discovery to production. That’s 15 years of drilling, development and mine building with no chance profit in sight - unless you sell your deposit to someone else who then has to find the capital to take it into production. Millions, sometimes billions of dollars are needed. There is no immediate return, there is no guaranteed return. Why invest in something with such long time horizons when you can invest in some tech play that will have its app uploaded to the app store, potentially generating revenue in a matter of months? The gains are quicker and the aggro is lower.

A lot can happen in those 15 years developing a mine. The metals markets can change, from supply shortages sending prices higher to glut sending prices lower. The money markets can change - interest rates can go up, for example. The political situation can change - politicians might seize strategic assets or impose windfall taxes, anti-mining lobby groups might block development, ESG narratives might take hold and prevent progress. It might be that after 10 years of drilling you discover the deposit is not quite as economic as you once hoped.

The Cycle Turns

Mining is hard. Many walk away. Then there’s no capital in the sector. With no capital, there’s no new metal supply coming to market. Then there’s a shortage of metal. Then, suddenly, we need to invest. Then capital floods the sector. It all starts to look rosy again. People make lots of money. Projects that will never make it to production start to get financed. Investors start to lose money. Rinse and repeat.

With Vladimir Putin’s invasion of Ukraine in 2022, commodities prices sky-rocketed. Supply chains were disrupted. Russian natural resources - and there are a lot of them - were now effectively off-line to the west. Nickel was probably the poster-child of the parabola. It suddenly spiked from around $17,000 to $100,000. The London Metals Exchange had never seen anything like it. Monday March 7th, 2022, was the date. That was the peak of the market. A bear market took hold. It has left the eyes of anyone invested in the sector bleeding.

It doesn’t matter if the metal being mined is base or precious, strategic or industrial, junior mining is in the doghouse. Metals prices themselves might not be that disastrous - gold is close to $2,000/oz. Copper is not far off $8,500/tonne. Iron ore is at $130/tonne. I’ve seen worse. The senior producers - the likes of BHP Billiton or Glencore - are not faring that badly either. It’s the juniors - the development plays, the explorers - that have been slaughtered.

There are exceptions. Uranium for example. We need uranium. Kazakhstan, the world’s largest producer, is struggling to get its uranium to market in the west. It has Russia to the north, China, which will not export, the east. Afghanistan and Iran to the south. Ukraine to the east. It’s geographically problematic. For that reason I like uranium and I think it’s going higher. But more than 90% of the mining companies in the uranium mining ETFs will not see any production for at least a decade, probably two. Taking a uranium mine to production is an even longer process than for most other metals. The ETFs might be going up, but the companies within them are drains of capital. The only compelling reason to invest in them is that the value of their resources are perceived to be increasing. I wouldn’t touch them myself. You are better off just owning the metal. Yellowcake (YCA.L), which stores it, is the way to play it.

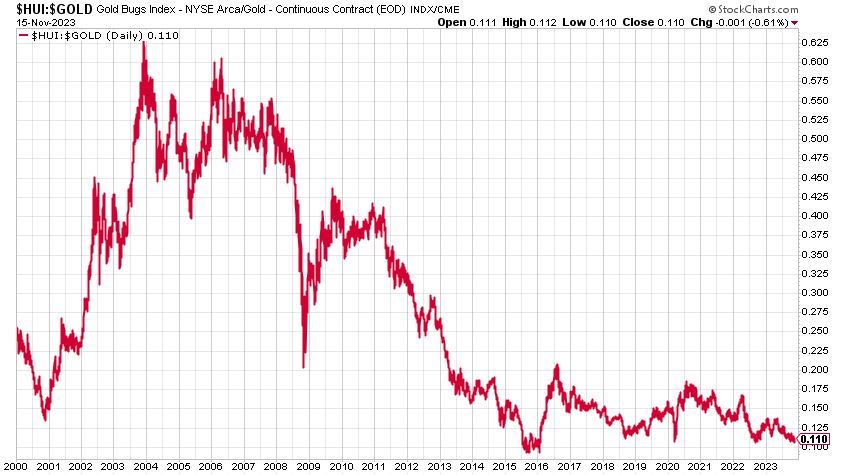

You could say the same for gold. Mining is supposed to give you leverage to the metal. That has not happened. This chart shows gold and the gold miners. When the chart is rising, miners are outperforming the metal. That has not happened in any sustained way for 20 years. The metal has been outperforming the miners. There are so many ways to own gold - ETFs, online bullion banks, futures, spreadbets, CFDs. Why take the individual company risk of a miner?

Though, on the positive side, there are signs we are making a multi-year double bottom.

If you are buying gold in these uncertain times, consider The Pure Gold Company, whether you are taking delivery or storing online. Premiums are low, quality of service is high. They deliver to the UK, US, Canada and Europe, or you can store your gold with them. I have an affiliation deal. More here.

The opportunity

The result of all of this is that there are junior mining companies that are currently offering extraordinary value. I’m not saying that in two months’ time they won’t be offering even more value. That is to say they’ve got even cheaper. They might well have.

But in any case here is a selection of four companies that I think have a good chance of doubling or tripling if and when this sector turns up.

Two of these are Canada listed. That is where most juniors are based. So if you are foolhardy enough to want to buy any of these companies, you will need a broker that deals in Canadian companies. (I use II, Interactive Investor. They have their shortcomings, but they are cheap. If you sign up with them, say I referred you – frizzers@gmail.com – and you will get a year for free, while I gets a referral fee).

Sierra Madre Gold and Silver (SM.V)

Sierra Madre Gold and Silver (SM.V) is putting a past-producing silver mine, La Guitarra, in Mexico back into production.

A fortnight ago it declared it has dramatically more silver than previously thought. Its mineral resource estimate went from 17 million ounces to 47.4 million ounces of silver in total (measured and indicated). This is a big development. The news came quicker than expected and better than expected. In mining it’s usually the reverse. The market barely shrugged. In a bull market this news would have doubled the stock.

Sierra Madre will be producing silver next year. Permits are all in place. The mine reconstruction is months not years away from completion. It needs silver at around $13-14 to break even. The silver price is $23-24, so it makes around $10 profit on each ounce. (It will end up being lower than that. It always is. But you get the point). The mine’s previous production was 1 to 2 million ounces per year. Sierra could produce at higher rates than previously anticipated given the increased resource, but even at the previous rate Sierra will make US$10-20m per year, which, for a US$36m market cap company, is pretty compelling. Anticipated production rates are: 800,000oz in year one, 1.3m oz in year 2, then 1.6m, 1.75m and 2.2mn by year 5. There is also potential to increase the resource when it drills out the eastern part of the property.

It is going to need to raise several million in the next few months, but CEO Alex Langer has that in hand. The next piece of the jigsaw is for him to demonstrate that to a doubting market. Then production hopefully by summer next year. Langer is buying. I have been buying too.

Andrada Mining (ATM.L)

Andrada Mining (ATM.L) is a play on both tin and lithium. It started out as a tin miner with lithium and tantalum bi-product, but lithium discoveries at its Uis project in Namibia have proved so compelling that the company re-branded itself as Andrada (after Brazilian mineralogist, Jose Bonifacio de Andrada e Silva, who first discovered the lithium-bearing minerals, petalite and spodumene). The lithium story has been suffering a little of late as the ESG narrative has lost its way, but this could prove a globally significant resource. In any case, though not that many seem to realise, the destiny of Andrada’s lithium is in the ceramics industry not batteries. Management is young and ambitious. The company is producing tin at profit. We are waiting for news on a big catalyst for the stock, which is its partnership with a “strategic investor”. There are, we gather, numerous applicants but this is a conversation that has been going on a long time. It’s a 5p stock. It could easily be 10 or 15p if this deal comes off.

Tharisa PLC (LSE.THS / JSE:THA)

Another cheap London-listed mining play is Tharisa PLC (LSE.THS / JSE:THA), which now has a market cap below £200 million. It has suffered because platinum group metals (PGMs) have been so out of favour, though it also produces significant amounts of chrome, which it ships directly to China at considerable profit, from its eponymous Tharisa mine in South Africa. Tharisa alone supplies around 10% of China’s annual chrome demand, and chrome prices remain strong.

The company has US$127 million in cash, and cash on hand of US$269 million including debt of US$142.2 million. Its dividend yield is currently around 9%.

The money is to construct its Karo project in Zimbabwe, but weak PGM prices mean it has delayed development by a year, which is unfortunate. Even without Karo, which the market appears to have deemed a liability not an asset, earnings per share for this year are roughly 32p, putting it on a PE of 2. Next year those earnings will be lower if the slide in PGM prices continues, so EPS will be lower. Then again PGM prices could rise. By the time Karo is producing you could be looking at a company with 400,000oz per annum of PGM and 2m tonnes of chrome production with decades of mine life. Huge. The market hates it. But it’s a bargain. If you are prepared to take on the risk of, one, South Africa and, two, mining.

Moneta Gold (ME.TO)

Oh, Moneta. Like an errant lover that promises heaven and delivers only heartache.

Moneta is developing the largest undeveloped gold project in North America - the Tower Gold project - near Timmins, Ontario. Its mineral resource estimate (MRE) showed it has 12.8 million ounces. With a market cap of C$100m, that means its gold is currently priced at US$6/oz. It is not unheard of for companies in such mining friendly jurisdictions to trade at ten times that. For example, nearby Marathon Gold, which has around 4m oz, has just last week been taken out by Calibre Mining, for an equivalent of around $60/oz.

But, with all the successful step-out and infill drilling that has taken place - it has put out something like 16 positive news releases in a row - that resource estimate is going to increase to, in my view, somewhere above 15m oz. But this is a huge project, a low-grade bulk deposit, and it needs bucketloads of capital to take it forwards. It also needs a new CEO. Chairman, Josef Vejvoda, is standing in as Interim CEO, while the search goes forward.

The investment thesis is that this asset is simply too big to ignore and that a major will buy it. My concern is that this story is so well known now - why has a major not already gobbled it up?

UPDATE: Right on cue we have this news of a merger. At first glance, this is not the big take out I was hoping for, but I’ll be back with more thoughts in the next day or two.

Final note

I’d love to tell you that a bull market is around the corner - cripes, it is overdue - and that these things are going to rocket. I can’t say that. I can say these things are cheap. But we are just going into North American tax selling season, when investors sell off their losers to take a tax loss. That is only going to add to the selling pressure. But the amazing bull market of 2016 began almost on the last day of tax-loss selling in 2015. Let's hope/pray for a repeat. Bull markets in junior mining tend to strike when you least expect them. Often they just happen with no apparent trigger. When they do happen, they happen fast and the moves can take your breath away. It’s often better to book your seat on the bus in advance.

This article first appeared in Moneyweek Magazine.

Buying gold?

My recommended bullion dealer is The Pure Gold Company, whether you are taking delivery or storing online. Premiums are low, quality of service is high. They deliver to the UK, US, Canada and Europe, or you can store your gold with them. I have an affiliation deal. More here.

How to get a SIPP, ISA and access to US or Canadian stocks

I use II, Interactive Investor, for all of the above. They have their shortcomings, but they are cheap.

If you sign up with them, say I referred you – frizzers@gmail.com – and you will get a year for free, while I gets a referral fee.

If you have signed up with Interactive Investor in the past, please can you drop me a line at the above email and let me know.

Disclaimer:

I am not regulated by the FCA or any other body as a financial advisor, so anything you read above does not constitute regulated financial advice. It is an expression of opinion only. Please do your own due diligence and if in any doubt consult with a financial advisor. Markets go down as well as up. I do not know your personal financial circumstances, only you do, but never speculate with money you can’t afford to lose.