We suggested a couple of weeks back that oil might due a hit as seemed the only sector that hadn’t been walloped and so it has turned out.

Both Brent and West Texas Intermediate slid back below $100 a barrel joining metals on the downward slope.

Metals have been battered even harder, of course, with silver – as often seems to be the way – leading the fall downwards.

How can silver be trading below $20 an ounce? How can platinum be below $850?

I’m not saying they aren’t going lower. They probably are. But there’ll come a time in the future when we’ll be wondering how on earth it was possible to buy these metals at these prices.

Silver below $20. Platinum below $850. Platinum is half the price of gold!

Remember when nickel went to $100k per tonne? It’s $21k now.

Wheat’s at $800. It was $1,300 in March. Corn, oats, soybeans, lumber – you name it, there’s pain.

Never underestimate the bust-to-boom-to-bust potential of raw material markets, I guess is the lesson. They always seem to return whence they came.

With this rout in commodities prices, this inflationary episode could yet prove to be transitory. (I stress I’m using the word inflation with its modern meaning: rising prices of goods in the CPI basket. The other kind of inflation – debasing money by creating too much of it – isn’t going anywhere).

The villain in the piece has been the US dollar. The dollar index is now at 107. Can it go higher? Maybe. It’s come a long way already.

June of last year we thought it had made a double bottom at 89-90. 103 was the huge line in the sand. It got through that at the second attempt. 120 is the next big one. It really would be an outlier if it got there – but this is a time of outliers.

The euro is now $1.01. Parity beckons. In 2000, with the dotcom chaos, it got to 82c (this was also before it had fully launched across member states). Is it going there again? Again, it would be an outlier, but it’s possible.

The pound’s at $1.18. I wouldn’t rule out parity there either.

Could capitulation by the Bank of Japan mark the end of the dollar bull run?

But I will say this. “Long dollar” is a crowded trade. Everybody’s talking about it. When it turns – and it will sooner or later – there’s going to be a lot of money made on the other side of this trade. FX traders are going to be all over it. Long anything anti-dollar – gold, the euro, perhaps even the yen.

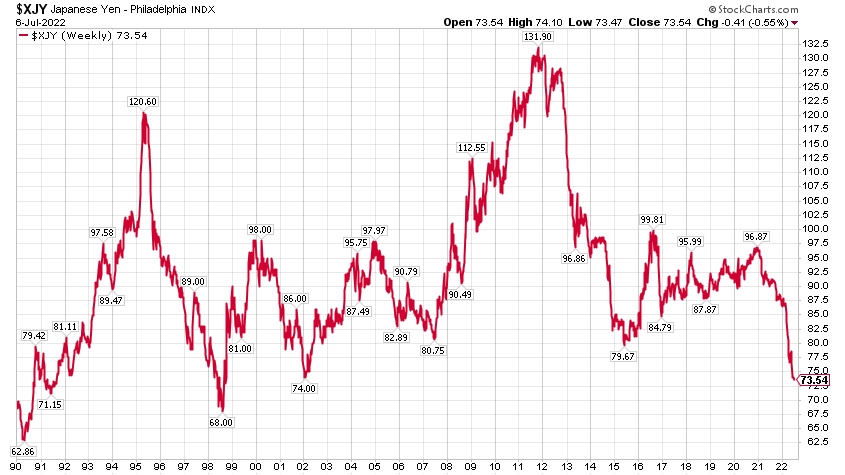

The yen’s at lows not seen since the Asian crisis of 1998. But could Japan have its own “Swiss bank” moment?

I’m referring to 2015, when Switzerland announced that it was going to abandon the franc’s peg to the euro (it was pegged at 1.20 euros to the franc) and the franc instantly shot up 20% as a result. That is an astonishing amount for a major currency.

The move destroyed many a forex trader’s fortune, not to mention the many people who had Swiss-denominated mortgages and other forms of debt. Many of them were from poorer nations with weaker currencies.

The yen is not pegged to any currency, but the Bank of Japan has committed to holding its benchmark 10-year government bond yield to 0.25%. With this so-called yield curve control, it pins down borrowing costs and “stimulates growth” (ergo cause asset price inflation - except that it hasn’t worked for years).

For decades now, shorting Japanese bonds (ie betting on higher yields) has been the mother of all widow-maker trades. I’m not ready to fall into that trap, even if Japan’s buying of its own bonds has gone nuts. The government now owns over 50% of its own bonds, and the rate of purchase has accelerated as it tries to hold the 10-year yield at 0.25%, even as the rest of the developed world starts “quantitative tightening” (ie doing the opposite).

Don’t fight the printers. You’ll lose.

But even with private sector savings exceeding the fiscal deficit and so much government buying, there is a possibility Japan has to stop defending the 0.25% mark. It may be because yields get too low relative to other nations’. It may just be that inflation pushes it over the brink (and a weaker currency means higher inflation).

But, cripes, there is some reversal in the yen (and thus in the dollar) that is waiting to happen.

Here’s the yen since 1990 (when the red line falls, the yen is getting weaker – the Y-axis shows how many dollars you can buy for 10,000 yen).

I don’t know when the dollar turns – but there’s going to be a mad scramble when it does.