Good morning,

As an experiment, today’s Sunday morning thought piece is in video. If you prefer, you can also read it below. You should also be able to read and listen, as many like to do.

Let me know what you think.

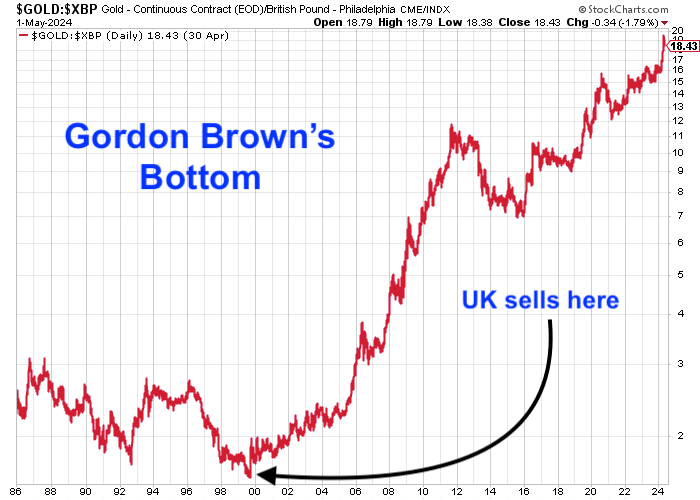

This week, May 7th, marks the 25th anniversary of one the UK’s greatest ever financial blunders. There is no shortage of them, but this one really stands out: that is Gordon Brown’s decision to sell more than half of Britain’s gold.

The decision and then its implementation were both of such cack-handed incompetence that for many the only possible explanation is conspiracy. We will come to that in a moment.

Every now and then the government does something that makes your ears prick up and think, “Well what are they doing that for?” This was one of those times. I knew nothing about gold or investing back then, but, even I, could see it was a dumb and needless thing to do. That’s the most amazing thing: Brown was under no pressure to sell. He was under no pressure to do anything. Even non-libertarians will struggle to explain why we need government when they are this incompetent.

It wasn’t just me. The tabloids said the decision was, “catastrophic.” Gold traders called it, “appalling”. Parliament was outraged. Foreign central banks were too. What was Gordon Brown thinking?

It was two years into Brown’s new job as Chancellor of the Exchequer. At the time, the UK held approximately 715 tonnes of gold, worth around $6.5 billion. The value of the country’s gold amounted to about half of its US$13 billion foreign currency reserves and the Treasury wanted to “achieve a better balance in the portfolio”. There was, it said, too much exposure to a single asset, which paid no interest and its price was volatile. Via a written question in the House of Commons the Government suddenly announced that it would be holding a series of auctions for its gold reserves, starting in six weeks, with an eventual plan to sell 415 tonnes by 2002.

Eddie George, the Governor of the Bank of England, raised “strong objections” as he and Gordon Brown clashed, but he was “outgunned by a coalition of the treasury and some of his own senior officials”.1 "The sale of the gold was not something that we recommended at the Bank,” George later said. “We did not think it was a good idea to sell such a large amount of gold at once. However, the decision was taken by the Chancellor and his advisors, and we respected their right to make that decision."2

London was still (just) at the epicentre of the gold market and its numerous gold traders thought the decision was nuts. Gold prices move in decades-long cycles, they told Bank of England officials, and the price was likely a lot nearer the bottom than the top. “The timing of the decision was ludicrous. We told them, ‘You are going to push the gold price down before you sell’,” said Peter Fava, then head of precious metal dealing at HSBC. “We thought it was a disastrous decision; we couldn’t understand it.”3 Revealing the timings and amounts for sale so far in advance would cause traders to short the asset, and that would drive the gold price lower.

Not only did Brown give a six-week advance notice to the market that the UK would be selling, driving away any potential buyers and sending speculators short in advance of the sale, the UK had even lent one fifth of its gold out, which speculators borrowed and sold in order to front run the UK’s sale. Sure enough, the price fell 10% by the time of the first auction in July to lows not seen since shortly after the US abandoned the gold standard in 1971. No wonder so many see this as the worst decision in British financial history.

Here is the timing of that first sale illustrated. £150/oz. Today we are at £1,900/oz. What a bunch of clowns.

As soon as the commitment was made, a consortium of central banks - including the European Central Bank and the Bank of England - signed the Washington Agreement on Gold in September 1999, limiting gold sales to 400 tonnes per year for 5 years. This triggered a reversal in price, a 25% rally in a week. Such gains have never been seen before or since.

If you are interested in buying gold, check out my recent report. I have a feeling it is going to come in very handy in the not-too-distant future.

In total, the UK eventually sold 395 tonnes over 17 auctions from July 1999 to March 2002, at an average price of US$275 per ounce, raising approximately US$3.5 billion.4 I have had it said to me many times that China was on the other side of the trade, but that is something we will never know.

Never explain as conspiracy that which can be explained by incompetence runs the wisdom, but this was so incompetent even those who favour that line of thinking struggle to explain Brown’s logic.

It was done to diversify UK assets, runs the standard explanation. Gold pays no interest, Brown wanted a yield. How was Brown to know interest rates would fall for the next 20 years? Many, especially on the left, supported the decision.

But such are the levels of incompetence, and it being gold, many other theories quickly emerged. It was “a political decision”, not a financial one, said the Bank of England.

Many argue that the sale was part of Gordon Brown and Tony Blair’s plans to take Britain into the new euro currency without asking voters: either to fund the euro itself, or to fund the UK's entry into the European single currency. This theory is linked to the wider belief that there is an agenda to create a European superstate that will replace national sovereignty. Hence the argument that the sale was part of a broader plan to suppress the price of gold. Brown was acting on behalf of a shadowy cabal of bankers and financiers, the same people that today are thought to be attempting to impose the Great Reset and control the world's financial system.

Others argue that he sold the gold at a low price in order to benefit his friends in the City of London. Brown is always suspiciously, in the eyes of some, quick to defend the “transparent” manner in which the sale was carried out. “The National Audit Office said that it was in a transparent and fair manner that the sale had happened while achieving value for money, so that is actually what happened,” Brown declared in 2007.5

Perhaps, simply, Brown thought the price was going even lower and called the market wrong. Not such an unlikely mistake to make. The 1990s had seen something like 1,600 tonnes sold by Argentina, Australia, Belgium, Canada and the Netherlands. Official sector holdings in 1968 accounted for some 40% of all the gold ever mined in history. By 1999, that figure had fallen below 25%. The new European Central Bank might not even bother keeping any bullion from the 11 founders of the forthcoming single euro currency. Analyst Kamal Naqvi, then at Macquarie Equities, told the FT: “The British are looking to sell before everyone else.”

Two months earlier, in April 1999, Switzerland, the fifth-largest holder of gold, narrowly passed a referendum to take the franc off the gold standard - it became the last nation to leave the gold standard. The sale of another 1,300 tonnes was green lit (Switzerland never actually sold). The following week the International Monetary Fund was “practically unanimous” in its plans to follow suit. There had been calls - led by Gordon Brown (who would repeat them in 2005) - to use the money to write off Third World debt for the new Millennium. “100 per cent debt relief on multi-lateral debt, IMF debt, to be written off by revaluing or dealing with IMF gold through sales,” Brown said.6

"The decision to sell gold was taken after extensive consultation with the Bank of England, and based on their advice that the price was likely to fall further. It was the right decision, and it released over £2 billion to invest in other assets".7

He was never a man to admit when wrong, even with reality staring him in the face. Once the decision had been taken he was too stubborn to go back on it, even with all that advice from the gold markets. The result was that he nailed the bottom of the market.

Of everything he did as Chancellor, internationally, this stupidity is what he’ll be most remembered for.

The mistake was to swap gold, the money of last resort, an asset that is nobody else’s liability, an asset with a track record as money going back to pre-history, for modern fiat money, beholden to the whims of others. Gold’s day was done, they thought. Professor Niall Ferguson declared the “twilight of gold”., whose only future was “as jewellery or in parts of the world with primitive or unstable monetary and financial systems.”

Hello!

Thanks very much for reading.

Until next time,

Dominic.

PS Here also in case of interest is my conversation with Tom Clougherty of the IEA from a fortnight ago. Enjoy!

"Bank governor in clash over gold sale'". The Guardian. August 6, 1999. Available online at: https://www.theguardian.com/politics/1999/aug/06/uk.politicalnews1. Accessed on February 27, 2023.

George, E. (2007) Eddie George, Former Bank of England Governor, in Commons Treasury Committee, 2 May [online]. Available at: https://publications.parliament.uk/pa/cm200607/cmselect/cmtreasy/uc69-ii/uc6902.htm (Accessed: 20 February 2023).

https://www.telegraph.co.uk/money/investing/gold-hits-all-time-high-gordon-brown-blunder-cost/#:~:text=Why%20Britain%20is%20still%20paying%20the%20price%20for%20Gordon%20Brown's%20gold%20bullion%20blunder&text=It%20has%20been%20considered%20one,of%20the%20nation's%20gold%20reserves (Accessed may 1, 2023)

https://www.telegraph.co.uk/finance/personalfinance/investing/gold/5296526/Gold-Does-Gordon-Browns-regret-selling-half-of-Britains-gold-reserves-10-years-ago.html

"Brown says 1999 gold sale was right". Reuters. April 15, 2007. Available online at: https://www.reuters.com/article/uk-imf-brown-gold-idUKROB48540820070415. Accessed on February 27, 2023.

https://www.thetimes.co.uk/article/brown-calls-imf-to-sell-gold-to-cut-debt-t2f888lswxd

"Brown defends UK's gold sales" by BBC News, published on 7 July 1999. Available online at: https://news.bbc.co.uk/2/hi/uk_news/politics/392617.stm. Accessed on February 27, 2023.